Home >

on

Making the 2020s about long-term partnerships between insurers and local authorities

In recent years, the shifting risk landscape and change to the UK’s Ogden discount rate has led us to have real concerns that soft market conditions in the public sector insurance market are out of step with broader commercial market realities. We believe 2020 could be the point at which this mismatch in pricing expectations begins to impact into the market.

The public sector represents a different set of risks and exposures compared to commercial organisations, its diverse range of responsibilities creates a unique set of risks and vulnerabilities.

That unique risk profile is reflected in public sector bodies’ desire for long-term relationships with their insurers, which also allows public sector insurers to spread claims expectations (and soften the blow to pricing) over an extended period. These longer ties are also a major reason why the public sector is typically a step behind the commercial market in reflecting trading conditions.

Given the structure of the public sector insurance market it is vital that there is a better understanding of the changing patterns of claims frequency and severity that the public sector faces.

Claims outpacing rates

Claims patterns over the past 25 years show that high severity claims, in the £1.5-2m range and above, can take as long as five years or even longer to develop. We also know it is the public liability claims profile of the sector, which sets it apart from commercial risks.

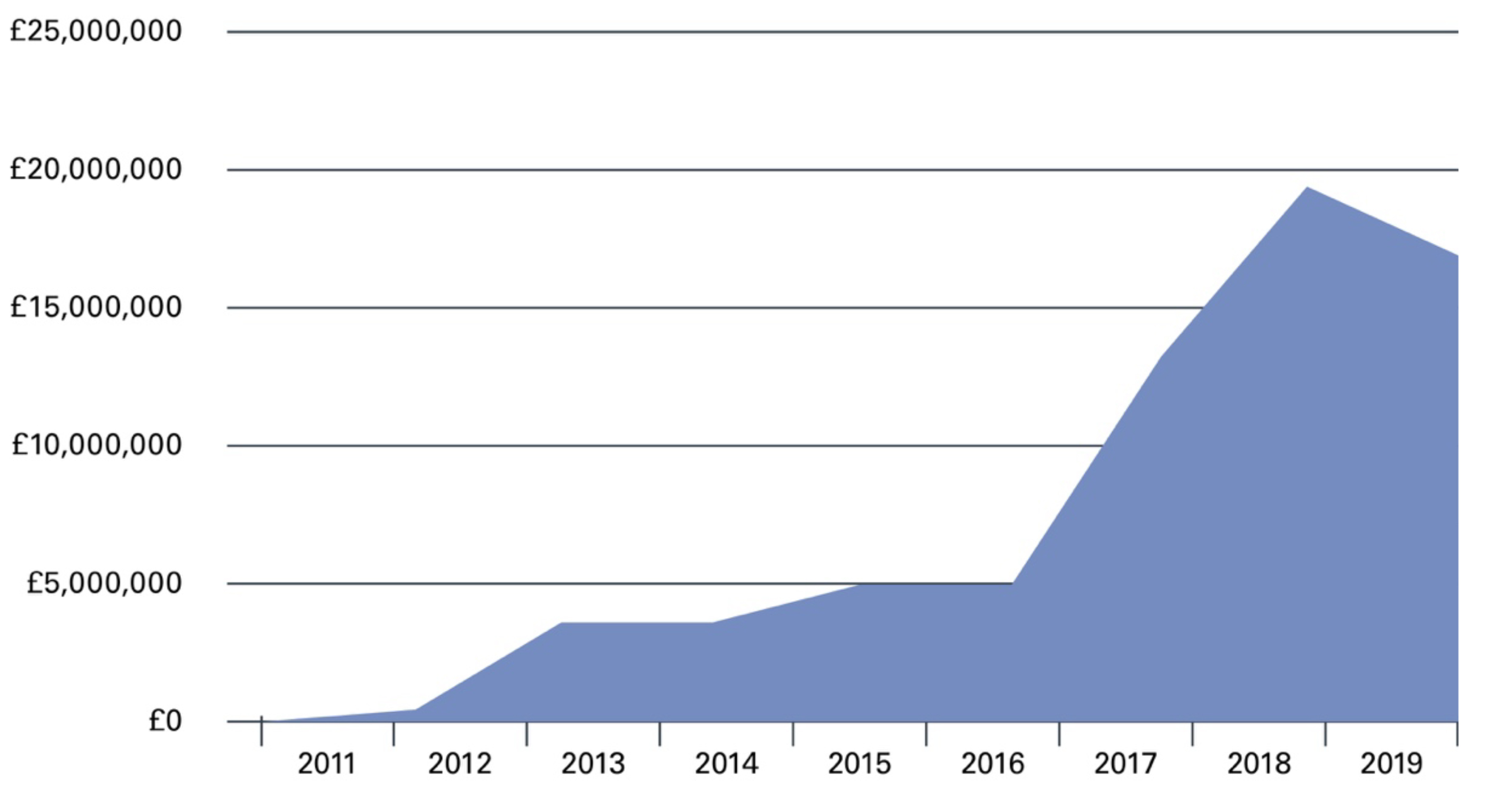

The graph below highlights so-called reserve creep since 2011 on an injury claim, approaching £17m over a period of eight years, despite insurers being aware of and on warning of the incident within days of it happening.

In many cases early reporting does not happen. Many liability claims, such as ‘failure to remove’ which affect children’s services, often have an incurred-but-not-reported period of 6-8 years. In a recent example of late reporting, we received a highway claim for a 10-year-old incident which is likely to settle for over £10m.

Having the ability to set parameters for a liability programme that is robust enough to settle liability and motor claims many years into the future, and at future claims values, is how RMP defines sustainability.

Premiums have not kept pace with claims inflation or substantial increases in claims severity and frequency for the period shown on the graph. While over the same timeframe, the lack of cyclical rate adjustment has steadily eroded insurers’ profit margins.

Long-term thinking is needed

The impact of persistently low premium rates combined with claims inflation is seen in a contracting appetite across commercial insurance lines from solicitors PI to UK casualty, motor and construction business. Further dilution of capacity is expected as insurers continue to exit poor-performing classes of business.

This impact has not yet been felt in the public sector market, but it would be naïve to believe it is insulated from the wider rebalancing act among insurers moving towards a more sustainable product.

The insured plays a role in this process by ensuring the tender process results in the best value for their business across the total cost of risk, including retentions and deductibles, not merely a scratch calculation based on premium.

History shows that there is nothing more expensive than cheap insurance. Public sector insurance buyers should bear this in mind when assessing of the sustainability of terms and the price of risk. Inevitably, when factoring in such factors, decisions will come down on the side of strengthening long-term relationships between insurers and local authorities

As a long-term partner, getting this balance right is vital to the obligations of an enduring relationship.

This article does not purport to be comprehensive or to give legal/insurance advice. While every effort has been made to ensure accuracy, Risk Management Partners cannot be held liable for any errors, omissions or inaccuracies contained within the document. Readers should not act upon (or refrain from acting upon) information in this document without first taking further specialist or professional advice.

Risk Management Partners Limited is authorised and regulated by the Financial Conduct Authority. Registered office: The Walbrook Building, 25 Walbrook, London EC4N 8AW. Registered in England and Wales. Company no. 2989025

Related Articles

Better collaboration for better infrastructure in the 20’s

The last 25 years have seen the completion of some spectacular infrastructure projects, what does the next decade hold?

Anytime, anyplace, anywhere: The transformation of working habits

Managing wellbeing and mental health is critical for the education system where the provision of support services has often been lacking.

Is sustainable construction possible?

UK housing trends have seen significant shifts during the past quarter of a century, a period which has seen the average house price escalate by more than 400%.

Stress in the emergency services – time to call 999?

Rushing to put out a blaze. Breaking up a nasty fight. Resuscitating an unconscious pedestrian.

Sign up to receive the latest from RMP

For information on how we use your personal data please refer to our UK Privacy Notice | EEA Privacy Notice.